So who's next for financial meltdown?

Spain, Portugal and Belgium set to follow Ireland into abyss as debt crisis threatens to destroy the euro

西班牙、葡萄牙和比利時準備跟隨愛爾蘭進入深淵,因為債務危機威脅會摧毀歐元

By Daily Mail Reporter

Last updated at 4:11 PM on 25th November 2010

Translation by Autumnson Blog

Belgium's debt reaches 100% of annual national income

比利時的債務達到 年國民收入的100%

Portuguese and Spanish borrowing costs rise sharply

葡萄牙和西班牙的借貸成本急速上升

Standard & Poor's reduces Ireland's credit rating to A

標準普爾降低愛爾蘭的信用評級至 A

Eire PM resists EU pressure to raise corporation tax

愛爾蘭總理堅拒歐盟壓力,去提高公司稅

Irish families each face 4,600 euro bailout bill

每一個愛爾蘭家庭面對4,600歐元救助帳單

Euro drops to a two-month low against the U.S. dollar over bloc's financial health.

歐元對美元跌至兩個月新低,對歐盟的財務狀況。

Report warns eurozone's problems won't stop at Ireland

報告警告歐元區的問題不會停在愛爾蘭

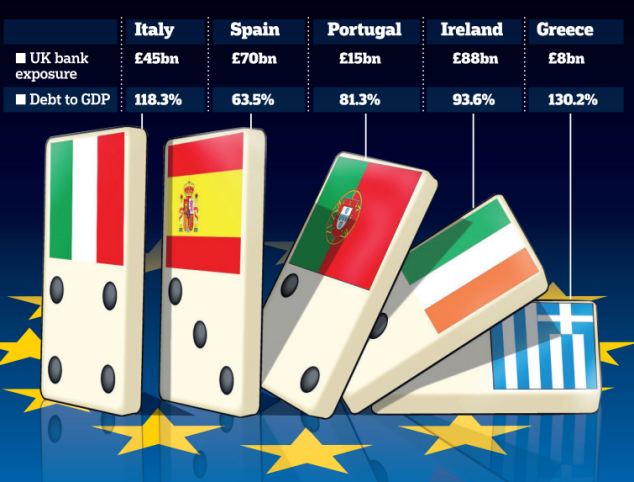

Contagion: Portugal, Spain and Belgium are viewed as the 16-nation eurozone's next weakest links

Contagion: Portugal, Spain and Belgium are viewed as the 16-nation eurozone's next weakest links傳染:葡萄牙、西班牙和比利時被視為 16個歐元區國家的下一個最薄弱環節

New fears have been raised about the future of the euro with the domino effect of faltering economies spreading today.

The latest nation to get sucked into the crisis is Belgium after market traders pushed the cost of insuring the country's debt to record levels.

The rising cost of Belgium's debt is now 100 per cent of annual national income. That is raising concerns the country could join Portugal, Spain and Italy on the growing list of countries that could be heading for a financial crisis along with stricken Ireland.

The eurozone was dealt a further blow yesterday after Portuguese and Spanish borrowing costs rose sharply as investors worried that their debt levels will prove unsustainable, putting them next in line for a European bailout.

As a major public sector strike in Portugal further undermined market confidence there, the interest rate on the government's 10-year bonds broke through the 7 per cent barrier yesterday. The 10-year Spanish bonds rose to 5.08 per cent from 4.91 per cent at the start of trading.

Portugal and Spain are viewed as the 16-nation eurozone's next weakest links now that Ireland has followed Greece and accepted a massive international rescue package.

Dominoes: The collapse of Greece and Ireland's economies could have a knock-on effect on other nations. Britain's public sector net debt is £845.8 billion, the equivalent to 57.1 per cent of GDP (gross domestic product, which is what the economy makes every year)

Dominoes: The collapse of Greece and Ireland's economies could have a knock-on effect on other nations. Britain's public sector net debt is £845.8 billion, the equivalent to 57.1 per cent of GDP (gross domestic product, which is what the economy makes every year)骨牌:希臘和愛爾蘭的經濟崩潰可能對其它國家有一連鎖效應。英國的公共部門的淨債務是八千四百五十八億英鎊,相當於國內生產總值的57.1%

The yields have been moving higher since Ireland accepted an EU-IMF bailout this week because investors demand a higher return for lending to countries with shaky finances.

Guaranteeing Ireland's solvency is also seen by EU governments, and officials in Dublin, London, Brussels and Frankfurt, as essential to protecting the euro as a currency.

There are fears across Europe that the Irish financial and economic chaos will spill over to other countries.

Portugal accounts for less than 2 per cent of the eurozone's total economy but a potential bailout for Lisbon would add to the pressure on Spain, the European Union's fourth-largest economy, and entail possibly dramatic repercussions for the entire bloc.

The euro dropped to a two-month low against the U.S. dollar yesterday on concerns about the bloc's financial health.

歐元兌美元昨天跌至兩個月新低,關注有關歐盟的財政健康。

Portugal's minority government has repeatedly insisted it doesn't need financial assistance because its austerity plan will drive down the country's debt burden.

While both countries are not at any immediate risk of bankruptcy, those rates are making their already heavy debt loads more expensive to finance. The higher cost to roll over debt is eating away at any progress the governments make in their public finances through austerity measures.

Traders are also worried Belgium's broken political system, which has left it without a government since April, is distracting it from tackling its worsening economic outlook.

Demonstration: Portuguese workers conduct a 24 hour general strike to protest against the government's austerity measures

Demonstration: Portuguese workers conduct a 24 hour general strike to protest against the government's austerity measures示威:葡萄牙工人進行 24小時的總罷工,抗議政府的緊縮措施

Out of service: A bus station in Porto is full up on Wednesday due to a general strike protesting at austerity measures aimed at controlling the country's current financial crisis

Out of service: A bus station in Porto is full up on Wednesday due to a general strike protesting at austerity measures aimed at controlling the country's current financial crisis退出服務:上週三在波圖的一個巴士總站放滿巴士,因總罷工抗議旨在控制該國目前財政危機的緊縮措施

The government of Yves Leterme collapsed in April after he failed to find a resolution to a three-year internal dispute between the country's Flemings and Walloons.

A report by a New York-based research and consulting company said that European officials don't expect the eurozone's problems to stop at Ireland and that a rescue plan for Portugal could be unveiled by early next year, when it is due to resume government bond sales.

為什麼普通德國人討厭救助歐羅

WHY ORDINARY GERMANS ARE SICK OF BAILING OUT THE EUROGerman Chancellor Angela Merkel is involved in the fight of her life (writes Alan Hall in Berlin).

Not against terrorists, the Left, or the French - but in trying to persuade her own people that the euro is worth fighting for.

Increasingly, as Germany bailed out Greece and will now have to dig deep to save Ireland, ordinary Germans are sick of it.

Long sceptical of swapping the mighty D-Mark for the common currency - a survey this year found more than 51 per cent wanted to ditch the euro before the full impact of Greece and now Ireland was known - there is an ugly mood abroad.

Burdened by high taxes, a harsh austerity programme and dwindling opportunities, they are in no mood for new lectures on why it is important to save the euro.

Chancellor Angela Merkel has yet to make an official statement on Ireland's request for help but the noises from the chancellery are that fear will play a large part in the PR campaign to convince Germans that the currency is good for them.

The word is she will sell up to £30billion worth of aid for Ireland claiming that social cohesion and peace itself in Germany will be threatened if the country doesn‘t cough up for Dublin.

But while she stokes up popular fears, she has plenty of her own. The climate is ripe in Germany now for a rightist party to grab up to 20 per cent of the voter from her conservative CDU on an anti-EU platform.

The recently formed Freedom Party is currently underway trying to do just that.

One caller into Radio Bavaria in Munich this morning said; 'If our cars and fridges and heavy machinery and chemicals and ships are good enough to be bought around the world priced in euros then they will be good enough to be bought in marks and to hell with the rest of Europe'.

But Eurasia Group said: 'There is a strong presumption that a package will be necessary for Portugal and the related planning is underway.

'Portugal will be pressed hard to accept a package even if the Portuguese government claims the country does not need it.'

Analysts have estimated Portugal will need at least 50 billion euros.

Spanish Finance Minister Elena Salgado also insisted Wednesday that Spain has no need whatsoever for a bailout like Greece and Ireland.

She said in a radio interview that the Bank of Spain's strict rules for the country's banks have ensured the Spanish financial system is healthy.

Though they insist their banking systems are in good order, the Iberian neighbours face similar challenges in reducing debt amid meagre growth.

Spain is struggling to emerge from nearly two years of recession, and unemployment is at a eurozone high of 19.8 per cent.

Portugal has borrowed huge amounts to finance welfare entitlements and private consumption.

At the same time it has protected jobs through outdated labour laws that make it difficult to hire and fire workers while industry has broadly failed to modernise and is chronically uncompetitive.

Portugal's austerity package, due to be introduced in January, cuts the pay of public employees by an average 5 per cent, trims welfare benefits and hikes income tax and sales tax.

The measures, including a reduction in state investment, are forecast to stifle already weak economic growth after a recession last year.

Despite the growing unease over the success of the Irish bailout and fears that Portugal or Spain might need help soon, a senior official said today the crisis will not lead to the breakup of the eurozone.

European Financial Stability Fund chief Klaus Regling said: 'There is zero danger. It's inconceivable that the euro would collapse.'

Mr Regling, who has overseen the eurozone's 440billion euro bailout fund since it was created last spring, said Ireland was not suffering from rampant speculation, but rather from a lack of buyers for its bonds.

'We're experiencing a buyer's strike, not wild speculation', Mr Regling said. 'And there's some uncertainty around whether the crisis will spread to other countries.'

Yesterday Ireland embarked on one of most draconian austerity programmes of any developed economy since World War II.

Brokers talk at the stock exchange in Madrid today: Spanish and Portugal's borrowing costs rose sharply yesterday as investors worried that the governments' debt loads will prove unsustainable, putting them next in line for a European bailout

Brokers talk at the stock exchange in Madrid today: Spanish and Portugal's borrowing costs rose sharply yesterday as investors worried that the governments' debt loads will prove unsustainable, putting them next in line for a European bailout經紀今天在馬德里的證券交易所說:西班牙和葡萄牙的借貸成本昨天急速上升,因投資者擔心政府的債務負擔將證明是難以持續,將他們放在歐洲救助線的下一位

Prime minister Brian Cowen unveiled plans to slash public spending by 20 per cent over the next four years to tackle the Republic’s soaring budget deficit.

The harsh medicine will include a 12 per cent cut in the minimum wage, nearly 25,000 civil service job losses and a punishing rise in the VAT and income tax rates.

Fianna Fail and the Greens launched a four-year, 15billion euro savings blueprint - equivalent to over 8,300 euro per household.

As Ireland battled to avoid national bankruptcy, estimates put the bailout bill for the average Irish family at 4,300 euros.

Brian Cowen, who is resisting calls to resign over the financial crisis, yesterday warned 'no one could be sheltered' from the cuts.

He rejected claims he will stand down after the 2011 Budget is unveiled in December to allow a new leader to fight the imminent general election.

Mr Cowen likened the agreed bailout to an overdraft as negotiations on exactly how the money can be drawn out continue.

He said in the Dail: 'We're talking about here, an overdraft, if you like. It's a contingency, it's available to us as required.'

Measures being brought in include cutting social welfare by three billion euro (£2.5bn), reducing the public sector pay bill by 1.2 billion euro (£1bn) and increasing VAT by two per cent.

The credit ratings agency Standard & Poor's has lowered its long-term rating on Ireland's financial reliability by two notches to A from AA- and warned that there could be further downgrades.

Painful cuts: Ireland's prime minister Brian Cowen, right, and finance minister Brian Lenihan announce the National Recovery Plan in Dublin today

Painful cuts: Ireland's prime minister Brian Cowen, right, and finance minister Brian Lenihan announce the National Recovery Plan in Dublin today痛苦的削減:愛爾蘭總理布賴恩考恩(右)和財政部部長布萊恩勒尼漢,今天在都柏林宣布國家復原計劃

However, the plan does not touch the country's ultra-low corporate tax rate - which contributed heavily to the so-called 'Celtic Tiger' economic boom, by attracting companies to the country.

Despite pressure from Germany and France, Mr Cowen is retaining his country’s controversial 12.5 per cent rate of corporation tax, which has attracted a slew of U.S. multinationals to Ireland’s shores over recent years.

The severe cuts equate to more than ten per cent of Ireland’s national income, compared with Britain’s plan to reduce public spending by about five per cent of output.Ireland’s ‘day of reckoning’ came as talks continued between the International Monetary Fund and the EU over a £72billion bailout.

Britain will contribute at least £7billion to the rescue.The Irish government has had to go cap-in-hand to the EU after escalating concerns over its finances threatened to capsize its crippled banking system.

愛爾蘭的四年計劃

IRELAND'S FOUR-YEAR PLANThe minimum wage being cut by one euro to 7.65 euro (£6.48);

VAT increasing one per cent to 22 per cent in 2013 and to 23 per cent in 2014;

Public sector workforce being cut by 24,750, bringing levels back to 2005 levels;

An increase in student fees;

Water metering brought in by 2014;

Carbon tax charges doubling to 30 euro (£25) a tonne

The country’s budget deficit is set to hit 32 per cent of national output this year after Dublin was forced to pump some £42billion into its stricken lenders.

Banking and economic experts across Ireland and Europe have raised concerns in the last 24 hours that it might not solve the problem.

There are also worries in some circles of a sustained bank-run by fearful customers.

Irish banks have already seen £19billion in deposits leave the country this year.

A statement in the National Recovery Plan said the measures would 'dispel uncertainty and reinforce the confidence of consumers, businesses and of the international community'.

It added: 'The tax and expenditure measures contained in this plan will negatively affect the living standards of citizens in the short term.

'But postponing these measures will lead to greater burdens in the future for those who can least bear them, and will jeopardise our prospects of returning to sustainable growth and full employment.'

Mr Cowen added: 'It's to bring certainty for our people.

'It's to ensure that they have hope for the future. To let them know that while we have a challenging time ahead, we can and will pull through, as we have in the past.

'It's a time for us to pull together as a people. It's a time to confront these challenges and do so in a united way.'

He said the plan would see workers facing taxes they paid in 2006 while the Government would oversee spending levels similar to 2007.

The Budget on December 7 will explain in detail how six billion euro (£5.1 billion) of the savings will be pushed through next year.

Mr Cowen rejected claims from backbenchers that he will step aside as leader of Fianna Fail before the end of the year.

EU Commissioner for Economic and Monetary Affairs Olli Rehn hailed the four-year plan as a ‘sound basis’ for negotiations on the final details of an international bailout, saying it struck a ‘good balance’.

But economists warn that the measures could consign Ireland to years of economic stagnation, making it harder still for it to repay its debts.

Ben May of Capital Economics said it faces an ‘insurmountable task of getting public debt down to a more sustainable level, which will eventually leave it no choice but to default’.

http://www.dailymail.co.uk/news/article-1332686/Spain-Portugal-Belgium-set-follow-Ireland-debt-crisis-threatens-euro.html

塔普利:'美國試圖摧毀歐元'

二次攻擊歐元僅僅是世界金融戰的序幕

意比等國形勢緊張 歐元區主權債務危機范圍擴大

西班牙每月1200名青年移居阿根廷逃避危機

沒有留言:

發佈留言